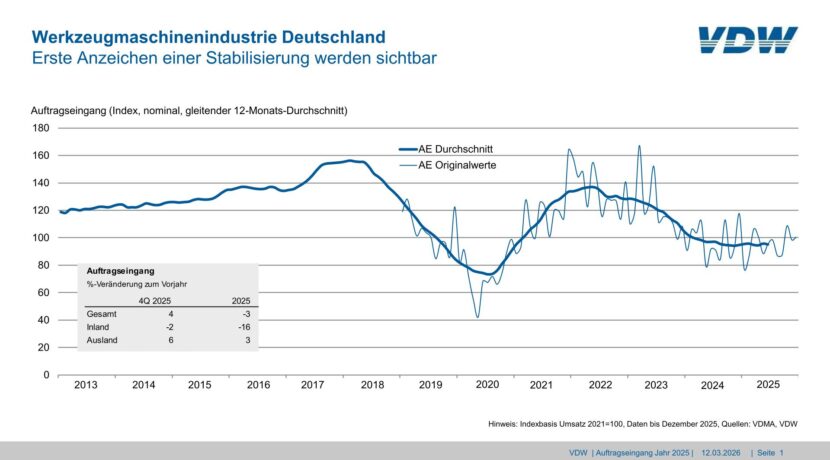

After two years of restrained investment, the German machine tool industry is showing early signs of stabilization. Order intake remains slightly below last year’s level, with a clear divide between domestic weakness and international demand. At the same time, data from VDW highlights a continued shift in global market dynamics, with China further strengthening its position in production, exports and consumption.

According to the VDW, incoming orders in 2025 declined by 3 percent compared to the previous year. This overall decrease masks diverging trends. While foreign orders increased by 3 percent, domestic demand dropped sharply by 16 percent. The weak performance in Germany reflects ongoing uncertainty in key customer industries, particularly the automotive sector and its suppliers.

Toward the end of the year, a slight recovery became visible. In the fourth quarter, new orders rose by 4 percent year-on-year, indicating a gradual return of investment activity. Nevertheless, production levels remain under pressure. German machine tool output reached €9.4 billion in 2025, still below the €10 billion mark and only marginally above the levels recorded during the pandemic years.

China consolidates global production lead

Global production continues to concentrate among a limited number of countries, with China further expanding its lead. In 2025, Chinese machine tool production reached approximately €30 billion, setting a new record. This corresponds to a global share of 37 percent. Germany and Japan follow at a considerable distance, with shares of 12 and 10 percent respectively. The United States and Italy account for 9 and 7 percent.

These figures underline the structural shift in global manufacturing capacity. While Germany remains one of the leading producers, its relative position continues to weaken as Chinese industry scales up both volume and technological capabilities.

Export shift and changing demand drivers

International trade patterns are also evolving. Global machine tool exports declined by around 3 percent to €41.4 billion in 2025. China surpassed Germany for the first time as the world’s largest exporter. Chinese exports increased by 13 percent to €8.6 billion, while German exports fell by 10 percent to €7 billion.

China also remains the largest global market, with consumption rising by 5 percent to €25.2 billion, equivalent to 32 percent of worldwide demand. The United States follows with €11.1 billion and a 14 percent share. Germany holds a 5.7 percent share, slightly ahead of India at 5.4 percent.

According to VDW Managing Director Markus Heering, growth impulses are shifting away from traditional sectors such as automotive and mechanical engineering. Instead, the industry is increasingly benefiting from demand in electronics and semiconductors, driven by digitalization, the expansion of artificial intelligence and the global build-out of data centers. At the same time, geopolitical developments and planned trade agreements, including those with India and Mercosur, are contributing to a realignment of international economic partnerships.